7TH EDITION

STATE OF THE COCOA SECTOR

THE COCOA POLYCRISIS Climate shocks, price volatility, and persistent poverty

Global Prices of Cocoa

The price of cocoa skyrocketed from USD 2,000−3,000 per ton in 2023 to over USD 10,000 per ton in 2025 and back down to USD 3,000 per ton in 2026.

This wasn’t just a spike – it was a seismic shift, and the market shows no signs of stabilizing. Prices are expected to fluctuate for years to come. Along with other factors, this causes great uncertainty.

Why Are Prices So Volatile?

The reasons are as heartbreaking as they are complex

Climate Change

Climate change is ravaging cocoa farms. Droughts, floods, and unpredictable weather are making it harder to grow cocoa.

Illegal Mining

Illegal mining is destroying farmland in West Africa. Cocoa farms are being bulldozed to make way for gold mines, leaving farmers with nothing.

Pest and Disease

Pests and disease are decimating crops. Entire communities are watching their livelihoods vanish.

The result? Less cocoa. Higher prices.

What happened next?

The price of chocolate went up. Demand went down. Production has rebounded, but chocolate is still expensive and demand remains low. More cocoa with less demand means lower prices.

Even during periods of high prices, farmers often fail to benefit as gains are eroded by inflation, extreme weather, and declining yields.

The Heart of the Crisis: West Africa

Côte d’Ivoire and Ghana, the world’s largest cocoa producers, are bearing the brunt. The 2024/25 season is a partial recovery, not a return to normal.

Ghana's bounce looks dramatic because it's rebounding off a low base; ~600,000 tonnes is still far short of its historic ~1 million-tonne output in 2020/21.

Production

Côte d’Ivoire

2023

+22%

2024

+2%

2025

Ghana

2023

+31%

2024

+55%

2025

Rest of the world

2023

+1%

2024

-1%

2025

Since farmgate prices are set before the harvest, Côte d'Ivoire and Ghana didn't benefit from the global price increase during the harvest. Less cocoa for only a slightly higher price means very little change in income.

In 2025, farmers finally got a high farmgate price. Meanwhile, global prices dropped. As a result, farmers in Côte d'Ivoire and Ghana could not sell their cocoa for the higher farm gate prices. Importers were looking to other countries where the cocoa was cheaper. Once again, the farmers bear the brunt of price volatility.

OVER

2 MILLION

TONS OF ALL COCOA

PURCHASED BY COMPANIES

ON THE CHOCOLATE SCORECARD

FROM DEFORESTED OR

UNKNOWN SOURCES

The European Union Regulation on Deforestation-free Products (EUDR) is on its way.

For compliance with the EUDR, cocoa needs to be traceable, geolocation mapped and confirmed deforestation-free.

For companies in the Chocolate Scorecard:

62% of cocoa is traceable to the farmer group.

55% is covered by a deforestation monitoring system.

65% is confirmed deforestation free.

These are all increases of around 10% since last year.

Traceability and Monitoring

are Possible

From 30 December 2026, the European Union's Deforestation Regulation — the EUDR, a new law that bans the sale in Europe of cocoa and other commodities grown on land cleared after 2020 — begins its first audit cycle. The first question auditors will ask is the simplest one: what percentage of your cocoa is verified deforestation-free?

All over the world chocolate companies have shown that knowing where every cocoa bean comes from — and refusing to buy it if a forest was cleared to grow it — is workable today. They can already answer the first question European auditors will ask.

What sets them apart is not the satellite technology — most companies have that. It is what they do after the satellite spots a problem. The leaders write supplier exclusion into their procurement contracts: if a farm has cleared forest, the company stops buying from it. They pair that with a reintegration pathway — farms can return once they have restored what was lost — and they ground-truth the satellite data so they don’t punish the wrong people.

Chocolate’s New Reality:

Shrinking Bars, Rising Prices

The ripple effect is hitting consumers hard

In the UK for example:

increase

+£3

Lindt gold bunnies already increased in price last year, and in 2026 they increased by another £3.

fewer eggs for a higher price

A 1kg bag of Cadbury Easter eggs (made by Mondelēz) contains fewer eggs while increasing in price by 35%.

100 to 90 grams

-10%

And it’s not just prices that are changing – products are shrinking too. Mondelēz reduced its Milka bars from 100 grams to 90 grams while raising the price by 50%. A 66% increase overall. It is called shrinkflation.

Are Companies Struggling?

Not Exactly.

Some Are Not

+8%

in net income

Lindt increased their profits.

They also increased consumer prices by 18%.

But Not All The Time

2025

a shock year

Hershey’s net income fell 60% in 2025 but has already rebounded with net income up 93.6% (Q1, 2026).

Companies

$241b

in revenue

Is what the seven biggest chocolate brands generated a combined revenue in 2025.

While farmers and consumers struggle, chocolate companies continue to grow and make profit.

How Are Companies Still Profiting?

Long Supply Chains

It can take years for cocoa to reach the final product. Companies are charging higher prices for cocoa they might have bought cheaply months or even years ago.

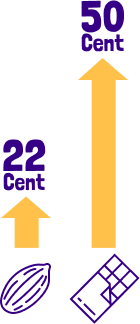

Cocoa is Only Part of Chocolate

Cocoa makes up a smaller part of the price than companies claim. For example, a 90-gram Milka bar contains 30 grams of cocoa. The cost of that cocoa increased by 22 cents, but the bar’s retail price rose by 50 cents.

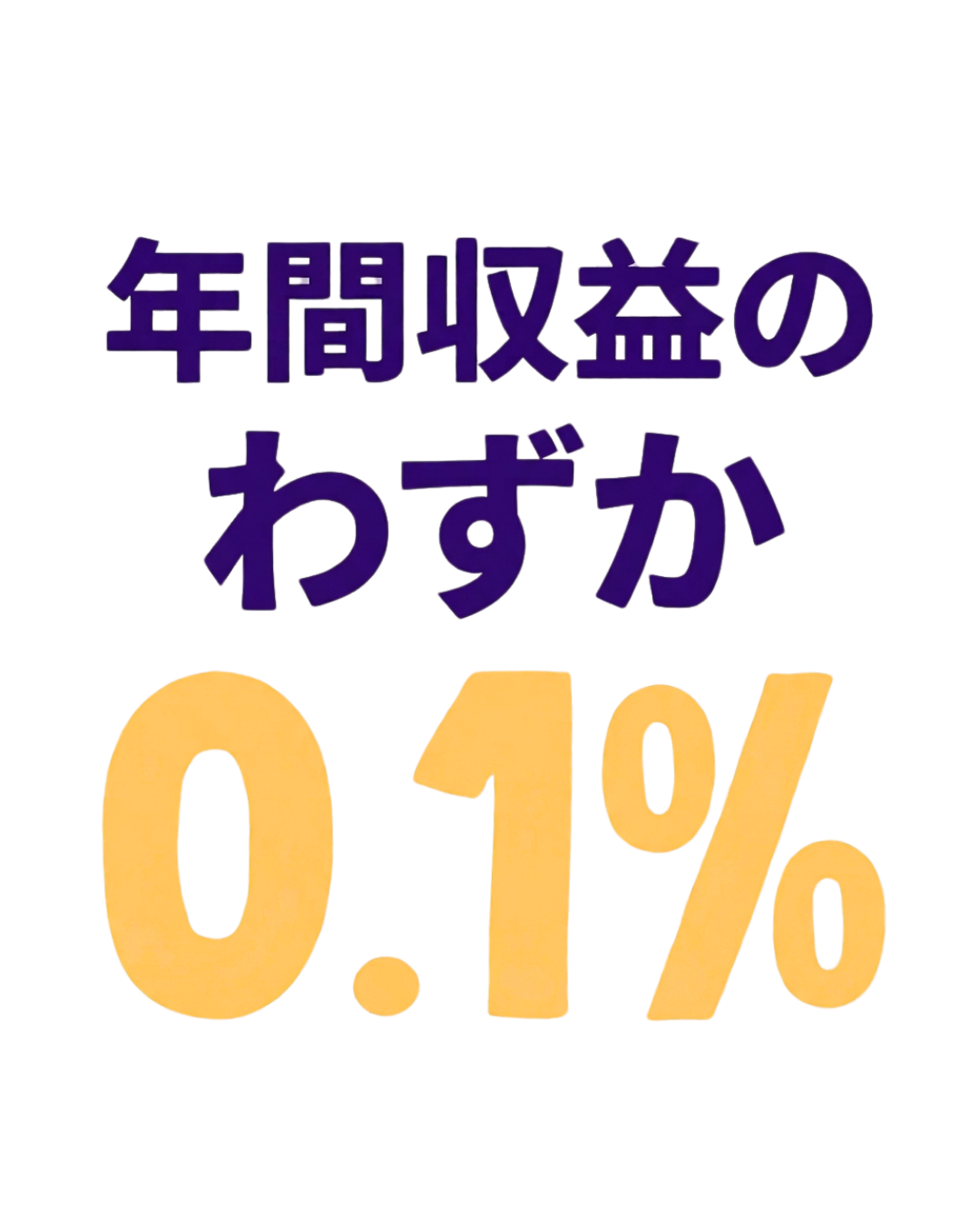

Negligible Compliance Costs

The cost of complying with the EUDR will only be 0.1% of annual revenue. The Corporate Sustainability Due Diligence Directive (CSDDD) will cost only 0.13% of annual shareholder payouts.

Passing on the Costs

Chocolate companies are simply passing the higher costs (and more) on to their customers or to the end-consumer to grow their profits.

COCOA IS

CHEAPER

AGAIN, WILL CHOCOLATE

FOLLOW?

The price of chocolate went up almost immediately when cocoa prices went up. Even though it can take over a year from cocoa to be made into chocolate.

Now that cocoa prices are back down, will the price of chocolate follow?

After passing the higher costs on to consumers, will companies now pass the savings on to consumers as well?

Retailers: Same Responsibility

Retailers

9 in 10 beans included 1 in 3 retailers willing to be measured. The Scorecard sits at the checkpoint nearly every cocoa bean has to pass through to reach your supermarket shelf.

When retailers sell their own private-label chocolate, they are chocolate companies in their own right. Eight of them have acted like it. Since 2021, Ahold Delhaize, Aldi Nord, ALDI SOUTH Group, Carrefour, Coop, MIGROS, Système U and Woolworths have shown up to the Scorecard every year — sometimes celebrating a green band, sometimes wearing a red one. They have engaged with uncomfortable findings on child labor, deforestation and farmer poverty rather than walking away from them. A low score with the lights on is more honest than a polished sustainability report behind a closed door. Showing up, year after year, is the first act of accountability.

The retailers leading on traceability haven’t reinvented the wheel. They’ve hitched their own-brand cocoa to suppliers who had already done the hard work. Coop routes through HALBA. MIGROS works through its chocolate subsidiary Delica AG with Cocoasource. Système U plugs into Cemoi-linked structures, including Transparence Cacao. ALDI’s CHOCO CHANGER and Ahold Delhaize lean on Tony’s Open Chain. The mechanism is the same in every case: borrow the discipline from a green-band supplier and let your private label inherit it. The route is published and replicable. Supermarkets don’t have to invent the solution — they have to choose to be part of one.

The harder half of the story is the silence. Eighty of the world’s largest chocolate companies and retailers were asked to be measured this edition. Forty-nine agreed. Thirty-one declined. Among the 32 major grocery chains we asked, only 10 participated. Twenty-two declined. That includes most of North America — Walmart, Costco, Kroger, Whole Foods, Target USA, Albertsons. It includes the European mid-tier band — REWE, Auchan, Leclerc, Casino, Colruyt, Metro — each publishing its own cocoa-sustainability commitments and each declining to be measured against them. It includes UK chains that have pledged “100% sustainable cocoa” on own-label and still declined to take the test on what that pledge means. Their internal reports describe transparency. The Scorecard, where transparency is independently checked, describes a blank row. Silence is not neutral. It is a choice.

Cocoa Production Areas